Published October 5, 2022

Home Prices and Interest Rate Trends In Charleston

A Look Back

Interest rates have been steadily floating between 3.5-4.5% for the past

12 years as we came out of the housing bubble of 2008. In January of 2021

the average interest rate on a 30year loan hit a historical low of 2.65%. This

was largely due to the COVID pandemic. If you were lucky enough to lock in a

super low rate at that time give yourself a pat on the back! The chances of

rates going that low again are pretty slim barring some sort of similar

event.

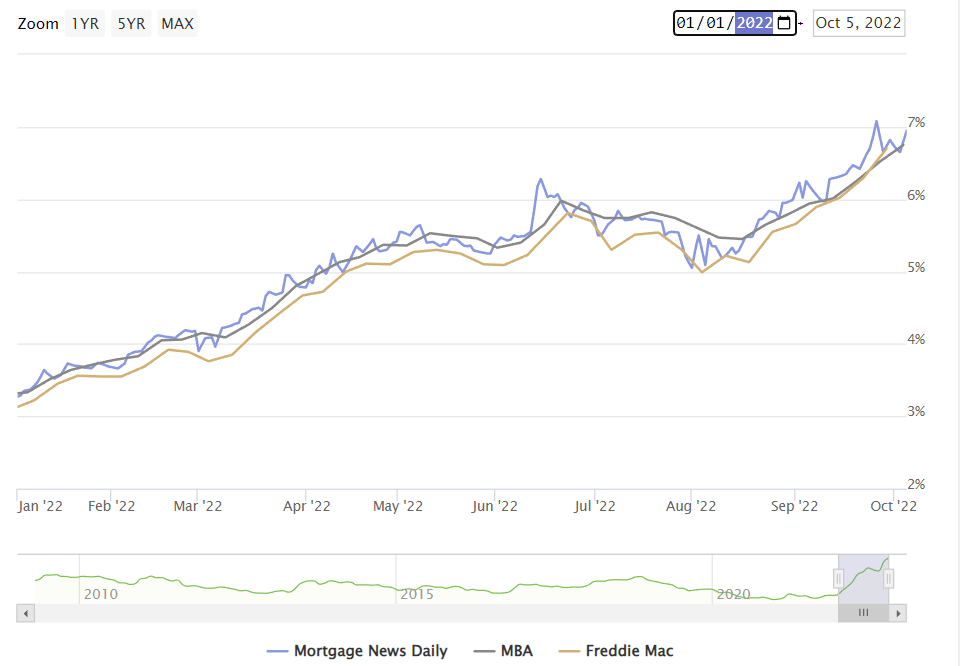

Over the past 9 months we have steadily watched our rates climb month over

month on average .3% from 3% to 7%.

Charleston was on a slow but steady increasing price trend and had/has

been for the last 5+ years thanks to a growing economy and influx of new companies.

When the pandemic hit things really kicked into high gear. The influx of buyers

and low inventory pushed our home prices to almost double their pre-pandemic

levels. The median Charleston County home

sale was 350K in 2020. That median sale price is now 525K.

Where are we now?

Currently, we are experiencing the highest interest rates we have seen

since 2008. They started climbing up, surpassing the pre-pandemic rates in Feb

of 2022. They have been continuing to climb and we sit squarely in the 6’s as I

write this.

Many buyers are asking, "Does this mean prices are coming

down?"

Theoretically, as interest rates go up one would expect

to see prices come down. Right? As interest rates go up, a person’s buying

power goes down and they can either not afford the amount they thought they

could or they cannot afford to buy at all. In response, buyers expect sellers

to lower their prices to keep these buyers in their buyer pool. We are seeing

this happen in many markets. Read More about this here.

Looking across the median sales price and interest rates

since rates surpassed pre-pandemic levels in February, we simply do not appear

to be experiencing price drops. We are seeing indicators of the market slowing,

no doubt, but prices have not been following along with the theory that

increasing rates will result in decreasing price.

Instead of coming down as rates have gone up, our prices continued to go up

until they peaked this June. Since then, they have bounced up and down within

10-15K of that peak. Here are the stats. I am separating New

Construction from resale just because New Construction companies manipulate

their inventory coming to market to manage pricing.

This is a look at the median sales price for resale homes in the tri-counties

over the last two years. Year over year prices are still up between 14-20%.

Prices peaked in June and since have fluctuated up and down less than 5% from

that peak since and appear to be leveling off.

This is a look at the new construction median sales price in the tri-counties over the last two years. Prices took a dip in June they bumped back up in July and hit a plateau in August and September. New construction should not be put in the same bucket as re-sale because they do try to control pricing by moderating other factors like available inventory, pre-buying mortgages, and offering various incentives.

What other trends are we seeing?

· Average number of

days on the market has consistently increased over the last three months from 3 to 11. Many neighborhoods I look at are seeing upwards of 30 days on market now.

· The average number of previously owned homes on the market has declined from a little over 1000 to around 900 since June. So fewer people that live here are looking to move. This is going to keep inventory tight and is more than likely not going to get better as home owners choose to renovate instead of upgrade to avoid the rise in interest rates. We will be dependent upon new construction to meet our inventory needs.

· The number of

showings per listing has continued to decline so we are seeing fewer buyers out

there.

· The number of

closed sales is down about 30% from the peak this year in May. With up

inventory and declining numbers of sales, this is just another indicator of

fewer buyers in the market.

What can we expect to see the rest of the year?

I do not have a crystal ball. No one can 100% predict what is going to happen in the future. If we try to apply some trend lines and predict the next 3 months this is what we get...

Since January the overall change in interest rate has been +2.1% with

rates going up on average .3% every month. The average purchase price

decrease over this entire time period has been 4700 per month.

Assuming rates continue their trend of going up .3% per month. We could

be looking at interest rates of 7.65+ and an overall decline of prices around 14K.

The Federal Reserve has been saying since early this year that they

believe an interest rate of 7-8% would help curb inflation and they wanted to

be there by the end of the year. This week we have crested 7% and depending on the economic report that comes out Thursday Oct 20th. Depending on whether it indicates inflation is decreasing or not will determine if the feds raise rates again in Nov. If they do, it will likely be another .5%. I would not be surprised if we are sitting at 8% going into the new year.

Experts are also saying that by this time next year we should be back to interest rates in the low 6’s and prices slowly but steadily appreciating, again mostly due to the lack of inventory. Read more here.

I bought this past year. Did I overpay?

The answer to this question is a resounding NO. If you bought this past year and your home value decreases by 50K from your purchase price you are probably still winning! How? Your interest rate. For example:

· Buying a 400K home

at 5% costs you $2147 per month and 773K for the life of the loan on a 30 year

fixed rate loan.

· If you had waited to

the end of the year, and you get that 400K home for 350K but you pay 7%

interest rate it will cost you $2329 per month and 838K for the life of the

loan.

So even if you feel like you overpaid for your home, you did not! When

you factor in the better interest rate that you received, you not only get a

better deal every month, you get a much better deal on the interest paid for

the life of the loan.

Advice for Sellers in this market...

For my sellers... if you were thinking of selling your home to cash out equity and downsize, you missed the height of the market to do that. April to June of 22 would have been the best time to do that. However, if you wanted to do this, go ahead and do it now simply because the value of your property will likely not see the significant gains that we saw of the last 2 years. The big difference now is that by waiting, your home has fewer buyers and it will likely take much longer than you may want in order to sell. You will want to make sure when you do go on the market that your home is in excellent shape, no condition surprises, and stands out from the other homes that are for sale near you.

If you were hoping to sell and roll your equity into a new home with a

larger mortgage, you are at a slight disadvantage because of the rise in

interest rates.

However, look at it this way… The days of 3-4% interest rates are gone. We will likely not see that again barring some kind of major event. The value of your home has increased

significantly over the last two years, you are in a great spot to sell and roll

over the equity, and with that equity you will have the cash to consider buying

down your interest rate. If you can, go ahead and do it. Get into the home you really want. If you wait until next year or longer you are still going to be looking at interest rates in the 6-7% range. Waiting is not going to change the situation around interest rates. You will likely be getting the most equity from your home now.

Advice for Buyers in this market...

Every situation is different....

For many, the question is, do you wait for that 20K price drop then buy? The information

presented above should tell you to not wait but there are some caveats to this.

If you are a cash buyer that does not need to sell your home … wait for

the lower purchase price. You have nothing to lose.

If you are a buyer that is financing, and you plan to pay this next home

off in the near future… It might be worth waiting for the lower purchase price.

When you pay off your home you are able to realize the interest savings and the purchase

price savings.

If you plan to finance this next home and it is not your forever home….

Buy now. Get an ARM or buy down points if you have the money to do it. Especially if you are currently paying rent. Every month you pay rent you throw money out the window when you can be putting that money into a home and gaining equity. If you wait a year or more to buy, you are still going to be looking at high interest rates. Why throw that money away when you could be building equity in a new home.

Everyone who is buying... you are in a much better position price wise than you

were a year ago. Sure your buying power is decreased due to the rise in

interest rate...but you do not have 10 other bids to compete with and you have

more time and slightly more inventory to choose from.

All of the numbers I have shared have come straight from our MLS. They are

averages and median. Once you start to dig into specific neighborhoods and

price ranges we may see varying trends….

Do you want to see

what your neighborhood stats are? Just ask!